Car companies’ “trading price for volume” strategy has led to a continued deterioration in the survival conditions of car dealers.

On August 18, the China Automobile Dealers Association released the "National Automobile Dealers Survival Status Survey Report for the First Half of 2025." This is the 17th time the association has conducted this survey.

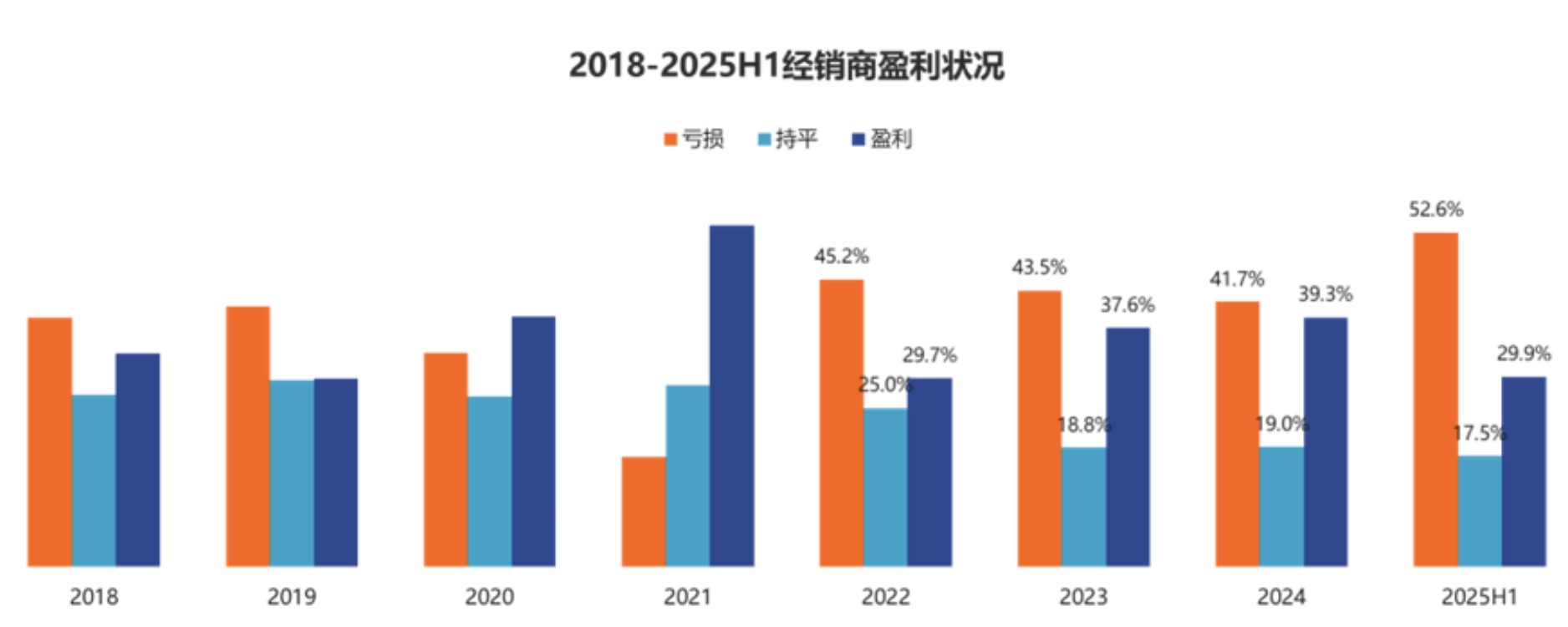

In the first half of 2025, the survival conditions of automobile dealers further deteriorated, and more than half of the dealers suffered losses.

The report shows that in the first half of 2025, the proportion of auto dealers experiencing losses will rise to 52.6% , while 17.5% will remain flat and 29.9% will be profitable. The proportion of loss-making dealers will increase by nearly 11 percentage points compared to 2024.

The China Automobile Dealers Association (CAA) analyzed that domestic auto consumption saw a modest recovery in the first half of the year, driven by policies to scrap and replace vehicles. However, fierce market competition has led manufacturers and dealers to slash prices to boost sales and compete for market share. This has resulted in a dilemma where sales are increasing but revenue is not, and revenue is increasing but profits are not.

Price inversion (i.e., the retail price is lower than the purchase cost of the car) is the main pressure faced by dealers and the direct cause of losses.

The survey shows that in the first half of the year, 74.4% of auto dealers had price inversions to varying degrees , and 43.6% of auto dealers had price inversions of more than 15%.

Severe price inversion has eroded dealers' working capital, leading to widespread complaints of financial pressure. This is particularly true for dealers of traditional fuel brands, where price inversion has led to significant losses in new vehicle sales. Dealers are facing difficulties in cash flow, and the liquidity crisis has spread throughout the entire distribution industry.

In addition, dealers also face challenges such as overly high sales targets and unreasonable manufacturer rebates.

In the first half of the year, nearly 70% of dealers failed to achieve their sales targets.

The survey results show that in the first half of 2025, only 30.3% of dealers achieved their sales targets . 29.0% of dealers achieved less than 70% of their sales targets, while 40.7% achieved targets above 70% but less than 100%. Looking at the target completion rates by brand group, luxury brands achieved slightly better targets than joint ventures and domestic brands.

In terms of dealer rebates, manufacturers offer a variety of rebate types, including basic rebates and fuzzy rebates. Fuzzy rebates account for a disproportionately high proportion, making it difficult for dealers to accurately calculate their actual rebates.

The survey shows that manufacturers' rebate cycles for dealers are mostly 2-3 months , with some manufacturers implementing quarterly assessments exceeding 3 months. Furthermore, only a few manufacturers provide full cash rebates to dealers' accounts.

It is worth mentioning that among new energy independent brand dealers (referring to stores that only sell new energy vehicles), 42.9% are profitable and 34.4% are loss-making, which is better than the industry as a whole.

This is mainly due to the fact that new car sales of new energy brands have performed better than fuel vehicles. In other words, the price inversion situation faced by new energy vehicle dealers is relatively mild.

However, it should be noted that new energy vehicle dealers also face significant challenges. The 34.4% loss rate should not be underestimated, and incidents such as the capital chain breakdown of Shandong Qiancheng Group, one of BYD's dealers, are not uncommon.

The survey shows that independent new energy vehicle brand dealers face pressures primarily due to low after-sales service value and long investment payback periods. Their after-sales service profits, financial insurance profits, and used car profits are all significantly lower than those of fuel-powered vehicles.

Under this pressure, auto dealers' satisfaction with OEMs declined again in the first half of 2025. The survey results showed that auto dealers' overall satisfaction score was 64.7, a significant drop from the end of 2024.

The China Automobile Dealers Association (CADA) believes the core issue lies in the accumulation of multiple operating pressures: a widening price gap has eroded dealers' profit margins, pushing them into deep losses. Increasing financial pressures have weakened dealers' ability to manage inventory. Even if the inventory ratio rises slightly above the warning line, already strained cash flow will be exacerbated.

In addition, dealers reported that manufacturers' rewards for achieving basic task goals have shrunk, and there is a serious imbalance between input and output. As a result, dealers' satisfaction with OEMs has declined significantly.

Looking ahead to 2025, dealers predict slight growth or flat sales, but their predictions for growth are lower than those at the end of last year. Approximately 49% of dealers believe sales will increase for the full year, while the proportion predicting a decrease has increased slightly compared to 2024.

"In the face of a poor market environment, dealers are actually constantly exploring the direction of business transformation, but they still face many challenges in the transformation process. For example, the pricing mechanism of 'Manufacturer Suggested Retail Price' cannot adapt to the current market, resulting in the problem of price inversion. Dealers are passive in this regard. This problem requires government intervention, promotion by industry associations, and active and effective measures from the OEMs to be resolved." said Lang Xuehong, deputy secretary-general of the China Automobile Dealers Association.

According to its official website, the China Automobile Dealers Association (CA) is a national-level corporate organization for the automobile distribution industry registered with the Ministry of Civil Affairs. Headquartered in Beijing, it is a national automotive service and trade industry association comprised of automobile (including used car) dealers, sales departments of automobile manufacturers, Chinese branches of multinational automobile companies, automobile auction houses, used car appraisal and evaluation companies, brokerage firms, auto parts and motorcycle parts dealers, physical auto markets, car clubs, auto detailing and accessories sales and service companies, car rental companies, local automobile distribution industry organizations, relevant scientific research and teaching institutions, social groups, relevant media, websites, and individuals.