Last week, Great Wall's Wei Jianjun said that the automotive industry has seen potential risks similar to those of Evergrande, but they have not yet exploded.

As soon as the words fell, BYD announced a new round of price adjustments. A total of 22 intelligent driving models under its Dynasty.com and Ocean.com were on sale for a limited time, with the highest subsidy of 53,000 yuan. Among them, the Qin PLUS DM-i Intelligent Driving Edition has a limited time fixed price starting at 63,800 yuan, the Haibao 06 DM-i has a limited time fixed price starting at 76,800 yuan, and the Seagull Intelligent Driving Edition has a limited time fixed price starting at 55,800 yuan.

BYD Qin L DM-i new energy electric vehicle at a sales store in Changzhou, Jiangsu Province, May 18, 2025.

As a leading company in China and the world's new energy, BYD, which has the pricing power for new energy, has once again launched a price war in an attempt to once again stir up the turbulent automotive industry.

This round of price cuts did receive a positive response from the industry. First of all, the capital market had a keen sense of smell. The price war directly caused the stock price to collapse, and pessimism spread.

On May 26, the A-share and Hong Kong-listed auto sectors collectively plunged, with BYD A-shares falling by more than 6% at one point. Seres, Great Wall Motors, Changan Automobile, BAIC Blue Valley, SAIC Group, and GAC Group all fell by more than 2%. In the Hong Kong stock market, the situation was even bleaker, with both traditional automakers and new car-making forces being affected, with Leapmotor, BYD, and Geely falling by more than 8%.

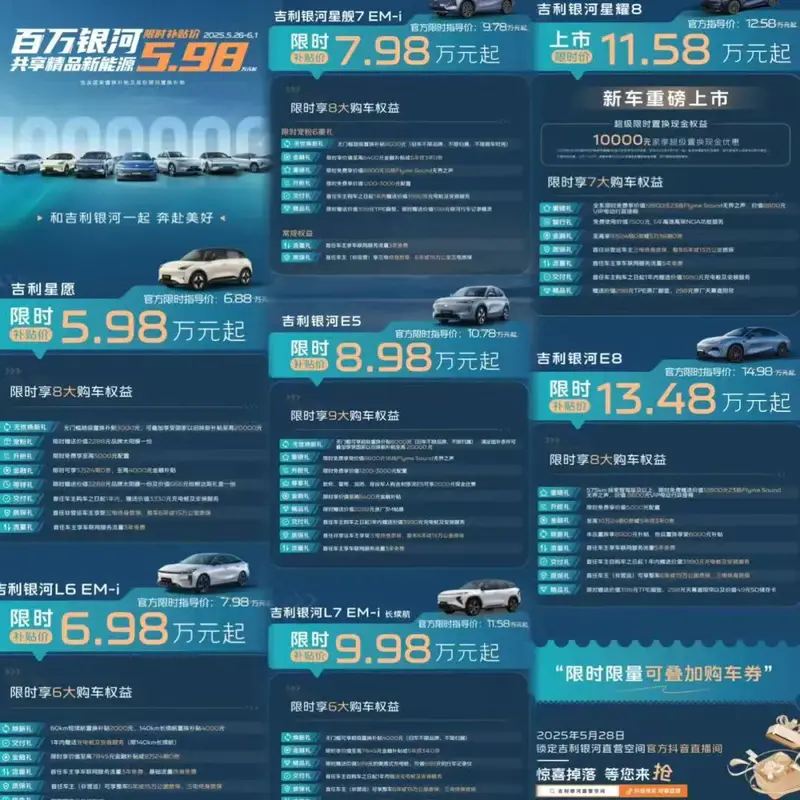

Soon, the trend of price cuts spread across the automotive industry. On the afternoon of May 26, Geely Galaxy also announced that it would join the price war, covering a number of popular models, with subsidies ranging from 5,000 yuan to 18,000 yuan. In particular, Geely Galaxy's popular model Star Wish, which originally cost close to 70,000 yuan, had its starting price directly raised to 59,800 yuan for a limited time. Other models such as L6, Starship 7, and E5 were also directly priced at 69,800, 79,800, and 89,800 yuan, basically competing with BYD.

If we say that sporadic price wars will not have much impact on the industry, at most they can be regarded as dynamic adjustments. However, as the big two, such as BYD and Geely, fight each other, it is bound to cause a great shock in the industry, and gradually lead the price war in the entire industry into deep waters. So far, Leapmotor, Zhiji, SAIC-GM and others have also announced their participation, and more companies such as Chery and Changan will be forced to join this fierce battle in the future.

Inventory is overflowing, and bloodletting is necessary

The term "one price" was originally used to describe joint venture automakers getting rid of their capital in the Chinese market and returning to the most realistic terminal transaction price. However, once the term was used widely, especially when leading automakers began to adopt the one price strategy, it meant that the Chinese auto industry was about to enter another competitive stage.

This price war was initiated by BYD, and soon the new force Leapmotor followed suit.

On May 25, Leapmotor released a Dragon Boat Festival poster saying that Leapmotor has launched a new one-price policy. The Leapmotor C16 Extended Range 200 Smart Edition is priced at 111,800 yuan; the Leapmotor C11 Extended Range 200 Smart Edition is priced at 103,800 yuan.

The two extended-range models are the entry-level models of their respective series. If the national replacement or scrapping subsidy policy is added, the maximum subsidy can be 20,000 yuan. The Leapmotor C01 only costs 94,800 yuan, the C16 only costs 91,800 yuan, and the Leapmotor C11 only costs 83,800 yuan. It should be noted that the size of Leapmotor models has always been large, which means that for less than 100,000 yuan, you can buy a C-class car with a length of more than 5 meters, which is really a bargain.

Next is Geely, which was mentioned at the beginning of the article. Standing at the critical node of cumulative sales exceeding one million and striving for annual sales of one million this year, Geely has to passively enter the market and stick to the expected share and market space. Especially in the market below 100,000 yuan, consumers are particularly sensitive to prices. More consumers who have no brand preference may turn to buy the model of the neighboring brand when faced with a price difference of 3,000 yuan.

In fact, the price war has already begun since the beginning of the year, especially BYD has cut prices several times. According to statistics, BYD has launched promotions three times since March. At the end of March this year, BYD Ocean Network and Dynasty Network launched a limited-time "one price" for some non-intelligent driving versions of entry-level models. The starting price of Qin L DM-i non-intelligent driving version was reduced by 10,000 yuan to 89,800 yuan, and the starting price of Song L DM-i non-intelligent driving version was reduced by 16,000 yuan to 119,800 yuan.

Secondly, starting from May 1, BYD increased the replacement subsidy standard for some intelligent driving models. For example, the comprehensive subsidy for the Han EV Intelligent Driving Edition, Han DM-i Intelligent Driving Edition, and Tang DM-i Intelligent Driving Edition starts at 35,000 yuan, including a manufacturer replacement subsidy of 15,000 yuan and a national subsidy of 20,000 yuan. The intensity of this promotion and the models involved are far greater than the previous two times.

The logic behind the price cut must be related to the company's own development pressure. Take BYD as an example. Dynasty and Ocean are BYD's core sales, but this year, many of its sales pillar products have been challenged by competitors and their market share has declined.

You should know that BYD's highest monthly sales volume previously reached 500,000 vehicles, but in the first four months of this year, BYD's average monthly sales volume was only more than 300,000 vehicles, and domestic sales volume was less than 300,000 vehicles per month. Although it still stands on the championship throne, it is far from the established goal, and many of its previous leading models have been overtaken by latecomers such as Geely Galaxy's more competitive models, and it has been forced to reduce sales.

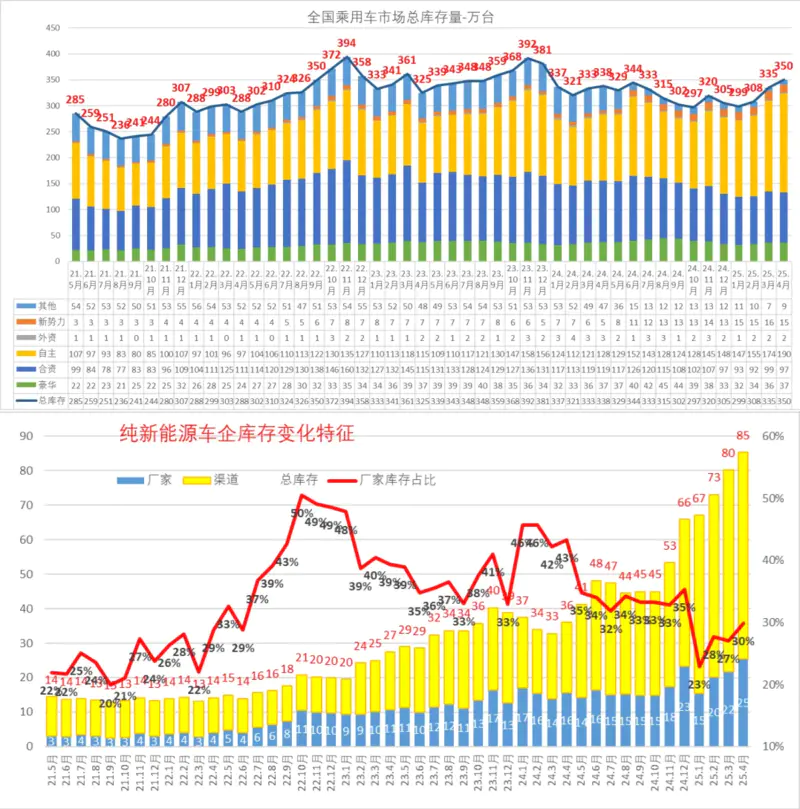

On the other hand, there is the issue of supply and demand balance. The inventory of terminal dealers has exploded. A week ago, the China Passenger Car Association released news that the inventory of passenger cars exceeded 3.5 million units, setting a record high for the same period in history. Among them, the inventory of new energy vehicles has reached a historical peak in recent years, at 850,000 vehicles, and the overall pressure continues to increase.

What do these inventory figures mean? Just look at the same period. No month in 2024 reached this value. The highest inventory in 2024 was only 3.44 million. Even at the end of April 2023, the inventory was only 3.25 million, and at the end of April 2022, the inventory was 2.88 million.

According to the inventory statistics of the China Passenger Car Association, the inventory in April must be reduced, because June to August is the traditional off-season for car sales, and dealers will not be able to hold on if the inventory is too high. If we consider that the entire car market grew by 7.9% from January to April this year, this means that under the subsidies, the consumption potential of car replacement has been almost released, and the subsequent growth will continue to be under pressure.

Another problem is that the new national standard for safer batteries and the subsidy policy for new energy vehicles are about to decline. If the inventory is not cleared in time, the older products will become a hot potato for manufacturers and dealers. So we can see why many car companies announced limited-time promotions this time, ranging from a week to a month. The core reason is to help terminals and dealers get rid of goods.

Price cuts are a double-edged sword

On the one hand, the backlog of inventory reflects the ambition of car companies to fully utilize their production capacity, and the production lines of new energy vehicles are running day and night like dumplings. On the other hand, in order to boost sales, some car companies use their production lines as money printing machines, but forget that the market appetite is limited after all. It's like a restaurant preparing food frantically, but the number of diners is unpredictable, and it is inevitable that overnight food will be thrown away.

On the dealer side, under pressure from inventory and sales, they certainly welcome this official promotion, because official publicity can stimulate wait-and-see customers to make decisions, speed up sales, and relieve high inventory pressure. Some leading brand dealers said that the current inventory coefficient is close to 3.

Of course, there are also optimists who believe that this price war will not last too long and will only be a dynamic adjustment for the entire system. However, at this pace, BYD, Geely, and new forces will inevitably disrupt the original price system order under the price war, and it is easy to form an impression on social media and consumers that the current car should be priced at this price, which will be a huge blow to the brand image, reputation, and old car owner ecology.

In fact, in addition to the price cuts caused by inventory pressure, price drops are also an inevitable result for car consumers under the current economic environment.

Especially since the old-for-new policy was introduced, passenger car consumption has shown a deflationary trend of "increasing volume and falling prices", which is caused by the increase in demand for mid- and low-end cars. According to common sense, when consumers increase their car purchases, they must be moving towards the goal of consumption upgrading. If they originally had an A-class car, they would definitely upgrade to a B-class car or SUV.

However, with abundant market supply, new energy, intelligence, larger space and more configurations, you can enjoy a better car experience than old cars by spending less money, which will undoubtedly push the price range of automobile consumption downward.

With large quantity and low price, the automobile industry has not received high-quality upgrades. After much investigation, it is found that the value of the industry has not been greatly improved. One of the key indicators behind the value is profit.

According to the National Bureau of Statistics, in the first quarter of 2025, the profit margin of the automobile industry was only 3.9%, lower than the average level of downstream industrial enterprises. In the previous year, in 2024, my country's automobile production and sales both exceeded 31 million, setting a record high. At this time, the profit margin of the automobile industry was 4.3%.

However, compared with the leading international automakers, the profit margin is quite low. The total profit of all listed passenger car companies in China is less than 40% of Toyota's annual profit. In an industry as high as the automobile industry, ultra-low profits cannot keep the industry continuously healthy and upward. Therefore, practitioners have only one feeling, that is, being overwhelmed and exhausted.

For consumers, short-term price cuts can indeed stimulate consumption and benefit them. But in the long run, this state of superficial excitement and internal distortion will have a severe impact on the entire industry ecosystem.

If car prices drop, manufacturers can still make profits and the industry ecosystem can be maintained in a healthy manner. This is indeed a core technology and competitiveness. However, if manufacturers want to reduce prices, the costs have to be spread across the entire supply chain. The pressure of payment terms and costs makes it difficult for the supply chain to be healthy. This is why Wei Jianjun pointed out: "What kind of industrial product can be reduced by 100,000 yuan and still have quality assurance? This is absolutely impossible."

More than a week ago, the top leaders of the National Development and Reform Commission said that "involutionary" competition has affected the high-quality development of the industry, distorted the market mechanism, and disrupted the fair competition order, and must be rectified. "Anti-involutionary" has been mentioned many times at the national level.

But the most realistic question is, despite so many calls for “anti-involution”, why is the industry becoming more and more involutionary?